In this blog, we focus on pension drawdown and how consumer expectations can be better met to help inform, prepare, and optimise their opportunity to meet their retirement goals.

The current environment has really put consumer retirement under the microscope, offering up challenges around how consumers can best meet their financial needs leading up to and in retirement.

3 ways that we can help consumers that are approaching or in retirement right now.

Better Communication

Following pension freedoms in 2015, a vast number of major providers are using deterministic forecasting to outline consumer retirement journeys. Although the Financial Conduct Authority (FCA) doesn’t currently prescribe an alternative, this does highlight income drawdown as an unrealistically attractive proposition when compared to an annuity. Without illustrating the downside risk, consumers are often left perplexed when a scenario unfolds like the 2020 global pandemic and subsequent economic crisis. Furthermore, without regular reviews and clearly defined investment strategies, it is almost impossible to set realistic consumer expectations throughout retirement.

So how can we immediately improve communication to consumers and members? Well, one option is “Clear and well-structured guidance and advice software”.

This software can help eliminate the ambiguity of lengthy and confusing written documents, providing clarity and reassurance that aids better understanding of the potential ups and downs that someone might experience when electing to drawdown on their pension. Find out more about advice and guidance software solutions here.

Better Investment Products

Rather worryingly, it is all too commonplace to use funds designed for accumulation in drawdown. The below example statement taken from the literature of a fund specifically used for income drawdown, “...the investment objective of the fund is to provide long-term investment growth...". "Target base rate + x% growth". Not only does this statement fail to inform the adviser or consumer of the income they can take, but it may also be inappropriate for income drawdown. It’s highly unlikely that this example fund was created with the purpose of drawing capital and income and again fails to effectively outline expectations. This is why the definition between accumulation and decumulation is so important. A fund that is based on growth for accumulation is highly unlikely to perform well under decumulation objectives. The volatility and sustainability of a drawdown fund must be clearly defined and the asset allocation optimised to meet that particular objective.

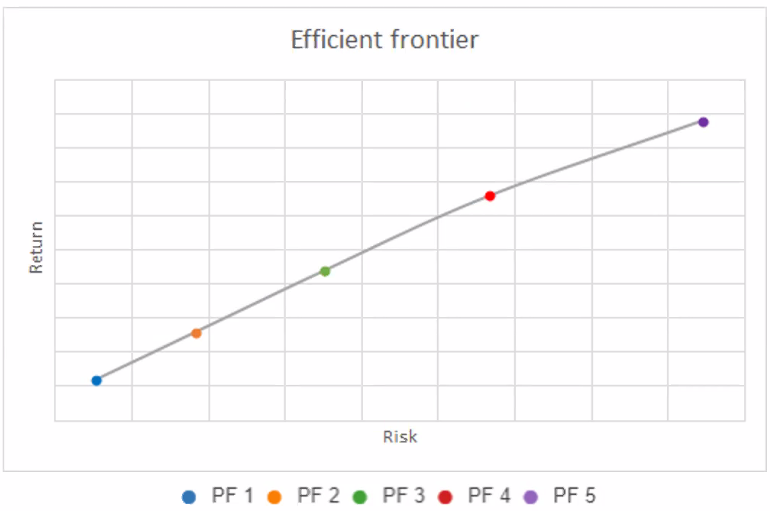

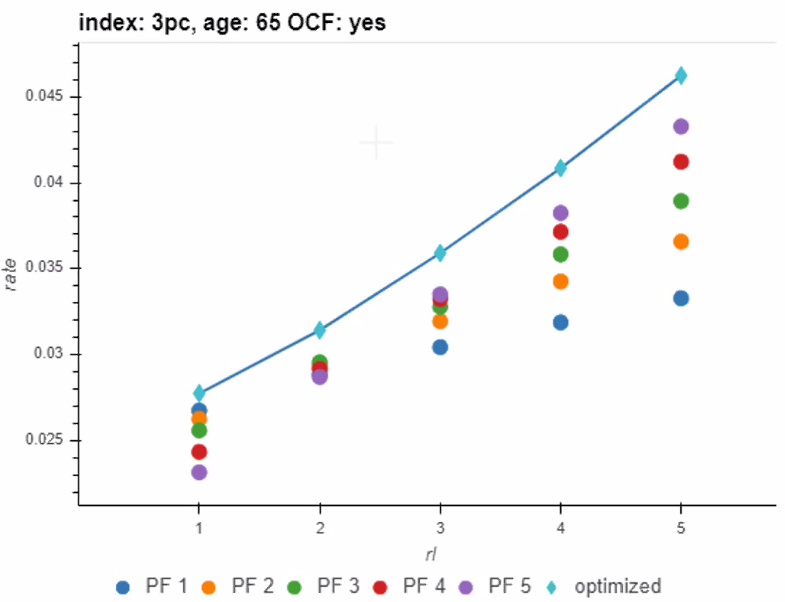

Graph 1 below illustrates an efficient frontier that is designed for growth and volatility. Over a defined term, the aim is to maximise the expected return on the underlying assets for a given risk. Graph 2 shows sustainable income levels for different likelihoods of achieving the associated risk level. This graph also plots the previously efficient accumulation funds where they are now measuring income and not the volatility of returns. This highlights how given a different objective, the efficient funds on one measure are not efficient on another measure. In fact, the risk ratings are almost entirely unrecognisable on Graph 2 from how they appear on Graph 1.

Graph 1

Graph 2

Better Modelling

Finally, and perhaps most importantly, the impact and effects of a failure to act before time will lead to irreversible implications for consumers. That is why modelling and specifically modelling for a sustainable income is such an important consideration when it comes to retirement drawdown.

In accumulation, losses can often be weighed against the opportunity for higher returns in times of volatility. However, in decumulation, if capital is eroded there will be less chance of proportionately replenishing those funds. This leads to implications such as sequencing risk, pound cost ravaging, and longevity risk often referred to as mortality drag. Find out more on how to avoid these various retirement planning pitfalls.

There are two main types of model that are most commonly used. The first which was eluded to earlier is a deterministic model. This is commonly used in advice and guidance tools but it is systematically wrong. Relying on fixed-rate assumptions, a deterministic model will only plot a direct path from ‘A’ to ‘B’ and makes no allowance for the aforementioned risks such as pound cost ravaging.

The second type of model is called a stochastic model and these are comprised of two different types; a mean-variance-covariance (MVC) and economic scenario generator (ESG). The MVC type model is still flawed because it is only based on a single set of assumptions about an asset class, its volatility and variance. Unlike an ESG type model, an MVC simply cannot tell you how it progresses into the future. Jablonski concludes, “Comprehensive, realistic, and forward-looking; a stochastic economic scenario generator is the only model that can comprehensively provide consumers and advisers with the tools they need to navigate the vast and changing retirement landscape”.

So what next?

Helping consumers to better understand their options in retirement and plan for potential volatility is all part of a realistic and forward-looking approach. Find out more about how you can illustrate financial planning that takes into consideration investment time horizons, and properly reflects term, the dependency of risk, and the return associated with different asset classes by reading our eBook ‘Modelling future outcomes. Why stochastic is the credible choice.’