In part one of this blog series, we discussed why investment decisions should be based on the most realistic assumptions as possible, and that should necessarily incorporate realistic behaviour of key asset classes. We highlighted the importance of two big direct features of our approach. These include reflecting the dynamics of the term structure of interest rates in fixed income investments and modelling the volatility clustering observed in equities to allow for the possibility of severe market downturns such as those experienced earlier this year. We believe that both have implications for long-term investment modelling.

In this blog, we will go into more detail about what this means for asset allocation and discuss our approach.

What does it mean for asset allocation methodology?

The interest rate-based model describes a term structure of risk for fixed income that allows for more risk to be taken over longer investment terms (typically around 1 to 2 times portfolio duration). What this translates to is that longer-term investors can take on more market risk than short-term investors, while still remaining on track for their risk preferences, and thus maintain the potential to reap higher returns later.

We employ stochastic volatility in our equity model to take into account the possibility of events like we saw in March this year with their impact on short-term investors and transactions as observed, while not assuming that such high levels of risk apply over the whole of the long investment term. This has similar effects on allocations to the fixed income modelling.

Using a long-term measure of risk enables a proportionate response to prevailing conditions in the model by explicitly allowing for other times. This means, importantly, that recent market volatility has little impact on the long-term risk measures used for portfolio optimisation but allows for valuations to do so. This has a stabilising effect on asset allocation while taking advantage of favourable pricing of assets for growth potential but not losing perspective on efficiency.

In short, having a long-term perspective better captures the view of risk and thereby allows for more growth-oriented investment, and this is what our approach seeks to do.

How is our approach borne out in practice?

It’s all well and good to be academic about some of these concepts but does our approach hold out in practice? Well, yes.

The response to the recent market crisis has been a case in point for us. Our approach delivered planned behaviour in the crisis in that:

- low risk investors were protected

- shorter term investors were protected (those with less time to recover losses)

- investors stayed in the market for the recovery

This provided validation of our approach to managing risk, accounting for investment horizon and investing in general.

By way of example, consider, the performance impact on our 5-level EValue portfolios targeting a long investment term (our lowest and highest risk portfolios are benchmarked to the expected volatility of cash and equity, respectively):

Figure 1: EValue Long-Term Asset Model Performance

Source: EValue as at 23rd October 2020. Past Performance is not a guide to future returns.

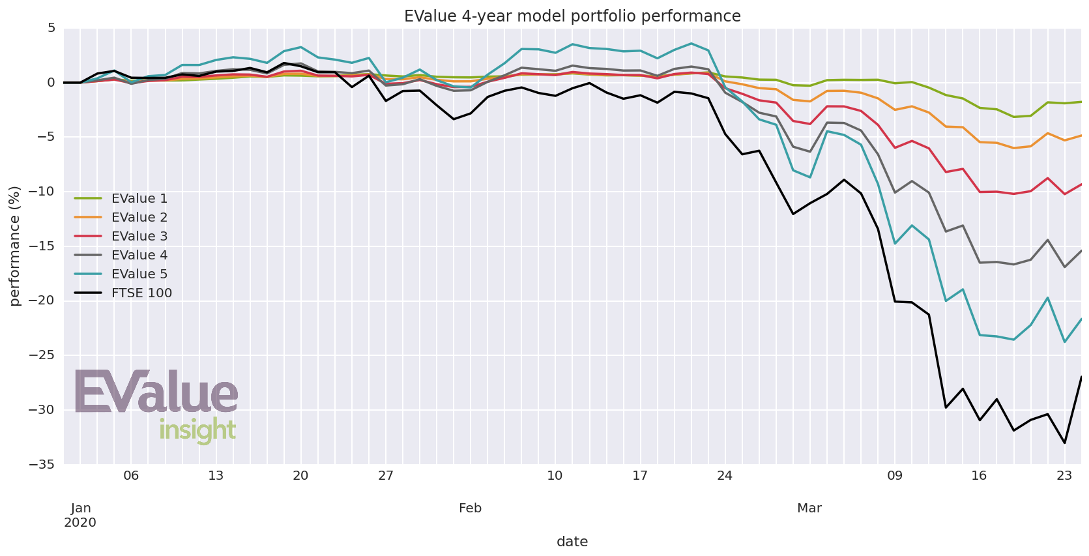

Low-risk portfolios were relatively insulated from the market turbulence, as expected from our approach to managing risk while the higher risk ones responded more directly but still less acutely than the market. At shorter terms, the portfolios were afforded relatively more protection than their longer-term counterparts, again as designed:

Figure 2: EValue 4-year Asset Model Performance

Source: EValue as at 23rd October 2020. Past Performance is not a guide to future returns.

The aim of our model is not to try and second guess the market but rather provide a range of outcomes that can be used as the basis for making asset allocation decisions. As such, our approach will not necessarily take investors out of the market at the top and bring them back in at the bottom but it will avoid the opposite in a panic, and it has delivered that in the recent crisis as we stayed in the market for the recovery.

There is more detail around how our approach fared in the recent market dislocation here.

How well has our approach done over time?

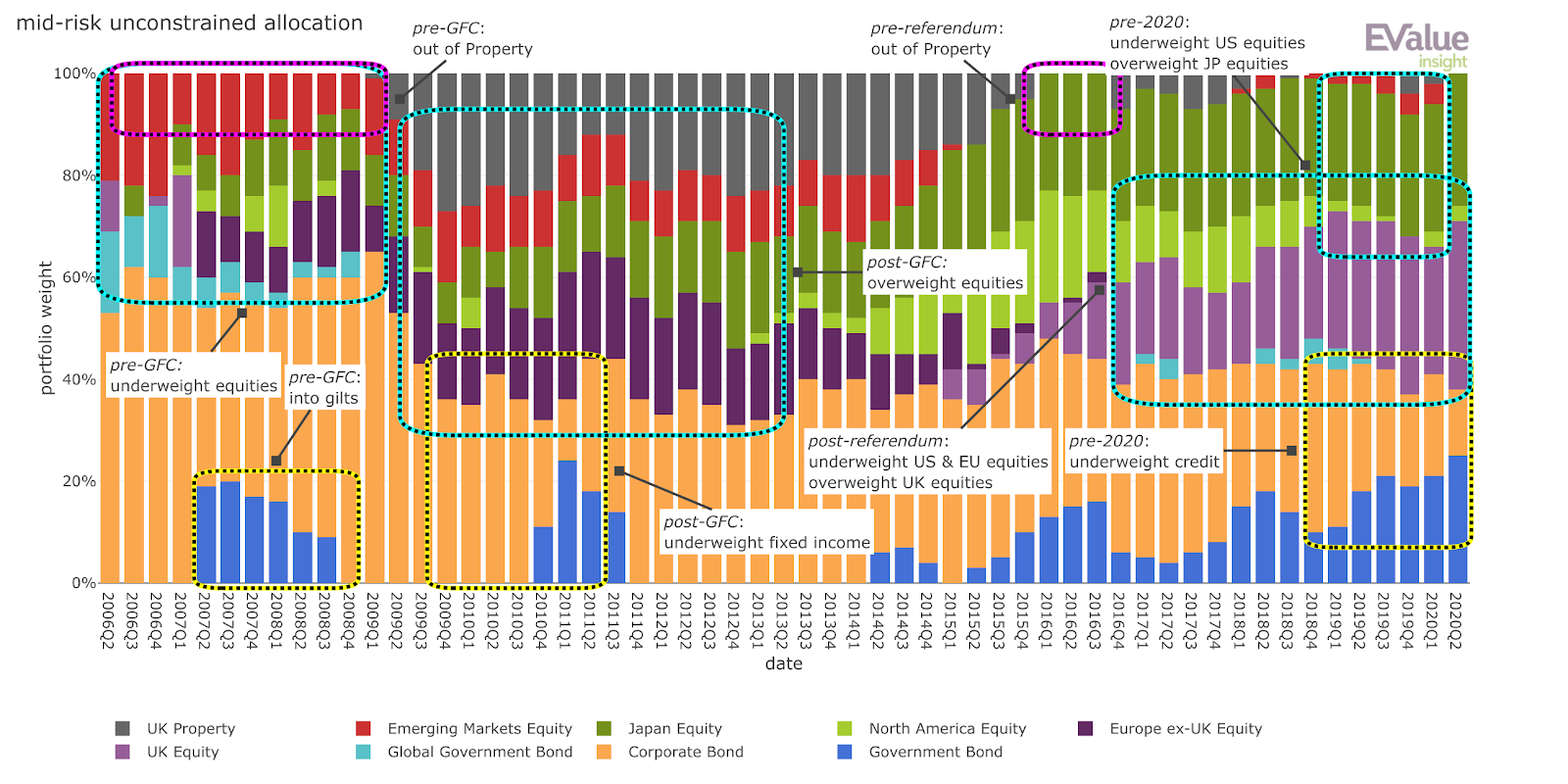

One way to test the efficacy of our approach over time is to look at what unconstrained asset allocations from the model reveal. Unconstrained portfolios expose the model in its rawest form as all our asset allocations are driven directly by the model; they are in effect “closest to the metal” (see chart below which shows asset allocation evolution for a mid-risk portfolio).

Figure 2: EValue Mid-Risk Unconstrained Allocation

Source: EValue as at Quarter 3 2020.

In the lead up to the Global Financial Crisis (GFC), the model proposed moving out of equities and into gilts which helped to lessen the impact of the market crash. It also suggested moving out of property pre-GFC which was also opportune. Once markets had bottomed, equities and property were back in favour to make the most of one of the longest bull markets in history.

In the last few quarters preceding the Brexit referendum, the model again suggested underweighting property, and thus avoided the devaluation that ensued. Following the vote, our portfolios were back in property to take advantage of subsequent gains. Sterling weakness and predominantly foreign earnings reduced the home bias enjoyed by UK equities and this was captured by the model which recommended its portfolio weighting be increased after the polls.

In the 12 months prior to Quarter 3 2020, the allocation to corporate bonds has been steadily decreasing while that to Japanese equities has been on the rise. This again positioned us well in the latest crisis in March 2020 as Japanese equities were the least worst affected of the developed economies and credit spreads blew up which was bad news for corporate bond holdings. Significant repricing also meant that UK equities were again attractive following the crash and the model suggested making the most of it in the April update.

All these features have been captured inherently by the EValue Asset Model and leveraged in our asset allocation methodology, yielding superior performance than our peers.

Conclusion

It is possible for all sorts of models to produce similar outputs at a particular point in time. The difference comes in how an approach deals with investments addressing different horizons and over time, and how consistently it responds to market movements. This is where our approach stands out from others as our explicit, transparent and data-driven approach ensures objectivity in investment decisions, and has proven to be a key driver in its success.

So what next?

Our range of strategic asset allocations is grounded in a set of robust and academically-tested investment beliefs that deliver outperformance by design. Our model has outperformed the market and other funds consistently for over a decade. This outperformance and resilience were especially visible during the Global Financial Crisis and during the Market Dislocation experienced earlier this year.

If you would like to get in touch or speak to a team member, please email us; contact@ev.uk