Now more than ever, vulnerability is a topic that all companies should be aware of, not just those providing financial advice or guidance services. And it’s essential to have robust processes in place to spot and manage your most vulnerable customers. The COVID-19 pandemic will have had a profound impact on vulnerable groups, so this topic is of particular poignance in the world we currently find ourselves in and looking to the future.

In this article, we will focus on how the use of technology can help you to identify, support, and engage your more vulnerable customers to ensure you can take the right actions, that provide individuals with the best financial outcomes.

What defines a vulnerable customer in financial services?

Let’s start by thinking about what being vulnerable means. The FCA defines a vulnerable customer as follows;

“An individual who, due to their personal circumstances, is especially susceptible to detriment, particularly when a firm is not acting with appropriate levels of care. The vulnerability can come in a range of guises and can be temporary, sporadic or permanent in nature.”

Put simply, an individual who fits one or more of the following criteria could be considered vulnerable.

- Low literacy or numerical skills

- Physical disability, or Long-Term Sickness.

- Mental health problems

- Low income and/or debt

- Caring for someone else

- Being older, potential loss of financial confidence.

- Being young, suggesting a lack of financial experience.

- Divorced / bereaved / job loss.

Why is it important?

Many of us will experience vulnerability at some point in our lives, and it’s essential to understand that often individuals in ‘vulnerable’ situations may not recognise it themselves. It means they may not immediately be forthcoming with the sort of information that will allow you to identify them as vulnerable, and also less likely to ring the alarm bell or know to ask for help. This is why a proactive approach to identifying these individuals is key, so you can then offer the appropriate support.

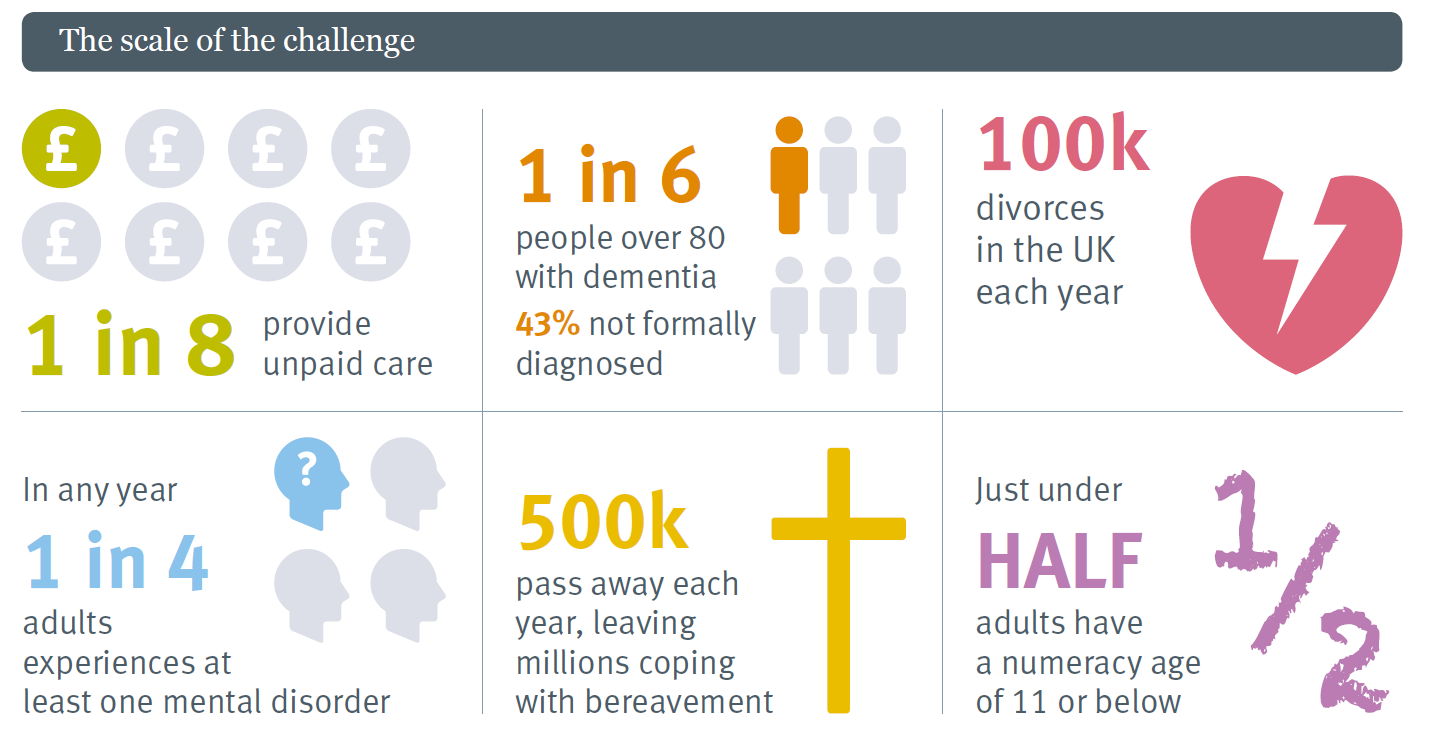

Did you know…

Source: Altus

So as responsible professionals, its important to establish processes to ensure that these customers are identified so you can continue to generate the best outcomes for them, and help them make informed decisions about their finances.

In its Occasional Paper No 8, the FCA made clear that firms must come up with a vulnerability policy, that should be robust, reflective of the times we live in, and embedded into their everyday working practices.

By not ensuring you have created sufficient processes, you run the risk of regulatory implications and an increase in customer complaints. Both of which could lead to reputational damage.

How technology can help?

As part of the Altus Vulnerable Customers webinar series, Andrew Storey, EValue Propositions Director, explained how technology, digital and front-end engagement could help financial services providers identify people coping with vulnerability.

Check out a replay of the webinar here

Identifying a vulnerable customer

There are three key areas where technology can help you identify the vulnerability of your customer;

Ask directly

This might sound like an obvious one, but ensuring you have the right types of questions to ask your customers, and importantly make sure you ask the questions at the right time. Start by asking simple questions such as ;

- Are you in poor physical health?

- Do you have problems with mental health?

- Do you have problems with numeracy?

- Do you have problems reading?

Many individuals may be more honest or comfortable responding to a computer, rather than speaking to a human - so bear this in mind.

Look for indications

For instance, has the customer used a pawnbroker, a payday loan company, or taken out a personal loan in the past 12 months. There are also indicators such as low financial assets, which then indicates vulnerability. All of those mentioned show that the customer may require a review, or their financial plan requires revisiting.

You can also use AI or Open banking data-driven analysis to check for unusual financial behaviour, such as random patterns of late-night spending. An example of this might be an individual making lots of unexpected purchases in response to stress, anxiety or depression, as a short-term coping mechanism.

Another indicator you could use is how a user behaves when using your tool. An indicator might be, excessive changing of answers or taking too long to complete responses, compared to standard user journeys.

All of the above indicators can help you identify characteristics that might prove a level of vulnerability.

Look for personal characteristics

Implicit psychometric profiling can also help with the understanding of a customer’s position. We have seen technology from Truthsayers, which allows an innate measurement of emotions or feelings towards risk that helps a to identify a customer as vulnerable.

The question style uses neuroscience to check whether you agree with a statement or not. We have been investigating how this could support risk profiling and can see how easily this can be extended to support vulnerable customers.

The speed of responses is a good indicator to whether the customer is anxious or not feeling confident, for example. By asking a range of emotional response questions, you will be able to build up a better picture of whether the customer could be considered vulnerable.

Support a vulnerable customer digitally through guidance or advice

There are many ways you can support your vulnerable customer through a digital user journey. The type of solution you may want to use depends on the style of vulnerability. For example, if the customer lacks confidence then providing simple education and ways to help them understand more fully can help them, or direct them to support services if they are suffering from high levels of debt.

Education

You can deliver education through a variety of options such as video, and communicate information in an easy to understand way through mini- tools or calculators. Much of these can be customisable to the individual, meaning a personalised feel.

Personalised Video

We would encourage the use of video. As you may be aware, we have developed an in house capability using our own unique personalised video technology which is used to deliver personalised videos to clients.

Providing educational videos for those at or near retirement which use our forecast APIs and a generic text to speech voice over can also be provided, and here are some examples we have already created:

- Basics - The impact of inflation on your savings

- Basics - Buying an annuity

- Basics - Choosing drawdown

We have been looking at how personalised video can be used to present results of advice back to the client in a digital environment. The following videos cover an example of how the graph of the income can be explained to a client by building it up one element at a time and how the results could be explained. This could also be used by an adviser or other support desk operator on a video call, mainly if the voiceover wasn’t included.

User testing has shown that the personalised videos have been very well received, and this is part of our roadmap for both guidance and digital advice. It can also be used by advisers to help them with the explanations to vulnerable customers. This is particularly important now that face to face meetings will be more difficult and therefore simple actions currently taken for granted such as drawing diagrams on paper will be much harder to do. Explaining the options using a video or similar with screen sharing will, we anticipate, become routine.

Design new products with vulnerable customers in mind

When bringing new products to market, you should consider the types of questions that vulnerable customers are asked e.g. accessibility, plain english, simplicity etc. This should be included as part of the development process to ensure these particular needs are met.

Online Advice for Vulnerable customers

We believe those vulnerable customers should be supported for advice by interactions with people. A level of human engagement can provide a level of emotional support that a computer cannot. A face-to-face or phone call is much more appropriate for these customers and will mean you can help them make informed decisions about their finances.

Conclusion

The COVID-19 pandemic will have had a profound impact on vulnerable groups that we have discussed. As we slowly begin to move towards a new normal, it is imperative for financial services offering guidance and advice, to assess the effects of the crisis accurately and to recognise the challenges that people are facing, in order to respond to their concerns effectively and ensure fair treatment of vulnerable customers.

We believe technology will play a crucial role in making sure you overcome these challenges. Not only helping you to identify individuals who are at the most risk, but also once you have recognised these customers, ensuring you can provide adequate support, taking the right actions that give them the best financial outcomes.

So what next?

Identify your vulnerable customers, talk to us about helping to understand what can be done to identify and support your processes for either guidance or advice. We can also help you understand how to monitor vulnerable customers in hybrid or digital advice with our extensive experience in providing different types of digital advice, please get in touch via contact@ev.uk